Credit Cards, Mobile Money and the Trust Gap

Why credit cards will never proliferate in mobile money-first economies and what mobile money must improve to expand digital commerce

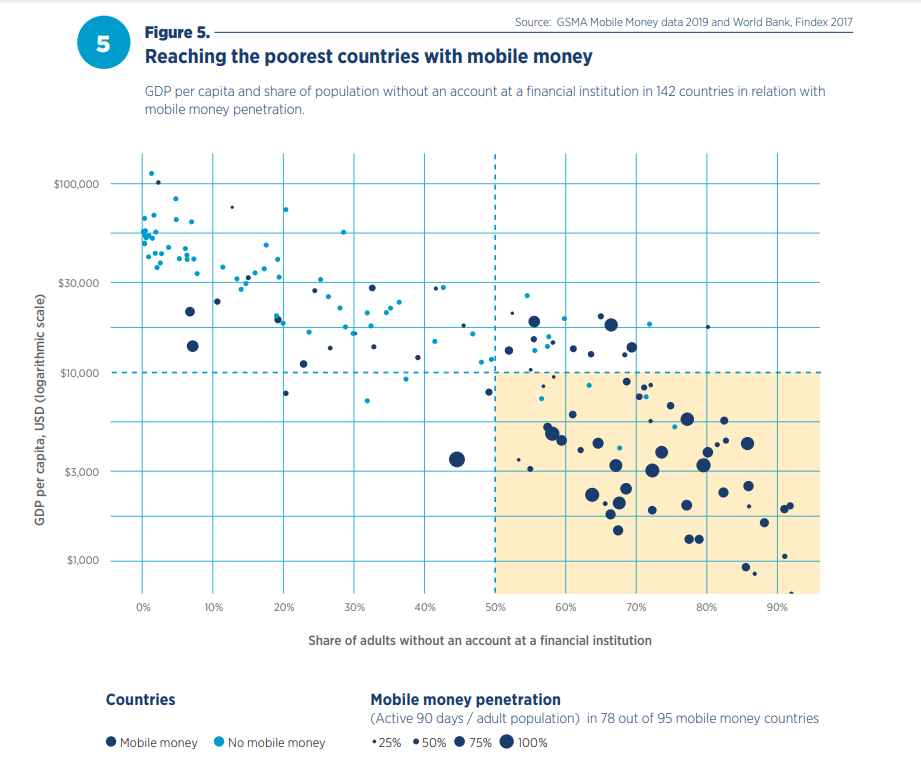

The prevailing globally accepted digital payment rails for consumer transactions are credit/debit card networks. This includes Visa, Mastercard, Amex, Union Pay and a few others. However, credit card acceptance has not prevailed in many emerging markets including Sub Saharan Africa (SSA), where less than 5% of consumers have credit cards. Meanwhile, mobile money has gained wide scale acceptance across many countries where there is limited credit card access.

Why did mobile money proliferate in SSA and other emerging market countries to the exclusion of credit card acceptance as the preferred digital payment rails?

Couple reasons:

1. Traditionally, credit cards (the post-paid kind) require bank accounts and most people in SSA do not have one. Furthermore, credit cards assume transaction risk by processing payments for merchants at the point of sale and then collecting from the customer at a later date. Assuming transaction risk necessitates an evolved credit scoring ecosystem, something not available in SSA. Even if you use debit instead of credit, you still need access to a bank.

2. Credit card networks are designed for transactions of certain minimum value. The interchange fees for card payments, including issuing bank fees, acquiring bank fees, network fees and others can add up. In developed markets, the average value of a card-based transaction can exceed $80 to $100 USD. Most transactions for mass market consumers in SSA may never exceed a few dollars. As a result, the fee structures do not make sense for the transaction values found in the mass market of SSA.

3. Credit cards require physical cards and Point of Sale (POS) machines to process payment. POS machines are expensive and the actual chip enabled cards themselves have a cost. The basic infrastructure for enabling credit card payments is too high for the average business in SSA. If your monthly sales don’t exceed a few hundred dollars, why would you invest a few hundred to accept credit cards for which most people don’t have access to anyways?

4. Credit cards are not designed for P2P (person to person) payments (i.e. sending money to your mom in a village), a critical unmet use case in emerging market economies. P2P payments are typically bank-led in developed countries. However given that most people in SSA are unbanked, any mass market payment rail would need to address this gap.

Mobile money addresses each of the problems with credit cards by creating a new set of digital payment rails that are independent from the prevailing bank and card-led systems in developed economies.

1. Mobile Money is always pre-paid, which means the mobile money provider is taking no risk paying a merchant or a receiver of funds. There is no credit risk so no need for credit scoring of the consumer. Furthermore, opening a mobile money account does not require a bank account, allowing any customer with proper identification and a mobile phone access to digital financial services.

2. Mobile Money fee structures are much more amenable to lower value transactions. Mobile money payment rails are not encumbered by the interchange fee structures required for card networks. Payments are routed directly to and from trust accounts held at local banks, incurring minimal cost. It will always be cheaper to process a mobile money transaction than a credit card transaction.

3. Mobile money transactions can fully take place on any feature phone. This means no acceptance device is required for the merchant or recipient of funds and no physical card needs to be carried by the remitter or payer of funds. Furthermore, QR codes can be used in combination with smartphones to avoid keying in numbers at point of sale so as to expedite payments without requiring investments in POS machines. By eliminating the need for POS devices, mobile money reduces the cost for merchants to accept payments.

4. The original use case of mobile money was P2P money movement. The transaction process is real time and does not require customers to open bank accounts.

The widespread proliferation of mobile money in many parts of SSA and Asia obviates the need for credit card acceptance so card networks may never be used by the mass market in these regions as is in developed countries.

While mobile money has key advantages over credit cards, there are also drawbacks. Addressing these shortcomings will be an important part of moving SSA digital commerce from its current early stage of development into a more mature digitally integrated economy. Three areas of further development include:

Deposit guarantee for Merchants:

Credit cards intermediate the availability of funds for merchants who need to guarantee delayed payment. In other words, by using a credit card to pay for something that must be charged after its use, the merchant is guaranteed funds will be available at the future time of payment. It is up to the card issuing bank to collect payment for the charge from the customer later on, the merchant is absolved of this matter.

One example is rental cars or rental equipment. Credit cards provide various mechanisms for the rental merchant to ensure sufficient funds are available when they charge the customer upon return of the asset. Without the credit card network intermediating this role, the merchant must make credit-worthiness decisions for each customer at the moment of each transaction, dramatically reducing the number of potential customers.

The flip side of this to address the concerns of the consumer is to develop escrow accounts that permit the customer to reject a product or service that does not meet the expected quality standards and return their funds back. An example of this is an e-commerce site that delivers a broken item. If the customer rejects the item, the funds are returned to the customer and the item is returned to the merchant.

Mobile money does not work this way, all transactions are pre-paid. There is no guarantee for a merchant that sufficient funds will be available at the time of return. As a result, all charges must be made upfront and in full. However, even this will not obviate the circumstance in which damage is done to the asset. The merchant will have no simple, low-cost way of recovering funds.

Mobile money providers must develop more advanced credit systems that address the risk for merchants who need payment guarantees in order to transact with unknown customers. For consumers, escrow account mechanisms can be established to bridge trust between merchants and customers in a digital environment where product and consumer are not present at the time of sale.

Rapid Transaction Reversals:

If you buy anything with a credit card, the transaction can be reversed at the point of sale by the retail sales agent without having to call or discuss with anyone.

Not the case with mobile money, which requires a reconciliation and reversal process that must be managed by a back-end office. This means point of sale transactions are difficult if not impossible to reverse. Let’s say you were overcharged for a meal. The restaurant would have to pay you back the difference in cash instead of going through the hassle of calling the mobile money customer service operation.

Mobile Money providers can develop more sophisticated charge back mechanisms that will allow customers to be refunded on the spot.

Recurring payments / Auto payments:

While the PIN requirement for mobile money does help prevent fraud, it also creates significant friction in the payment process of subscription payments or other recurring payments. Mobile money users must actively purchase subscriptions on a periodic basis. Scheduling payments to happen at a certain time, or authorizing automatic payments for a monthly invoice amount is not possible.

This is not the case with credit cards, which allow for consumers to permit merchants to process payments in regular intervals for undetermined amounts. For example, a post-paid cell phone bill can be paid by credit card through an auto payment for the amount of the invoice auto generated each month. This creates a level of convenience for the customer, and also reduces the cost for processing payments for the merchant.

Mobile money providers can develop systems to allow for regular subscription payment that address necessary permissions and allow customers more control in how they manage those subscription payments.

In a nutshell, mobile money needs to adopt the good parts of using a credit card - risk management, transaction reversal, trust intermediation - and leave out the bad parts - high cost, interchange fees, POS and card infrastructure requirements.

All the functionality described above is necessary for mobile money to expand beyond the core P2P and merchant payment / bill payment functionality it is primarily used for today. It is unlikely that traditional methods of payments (like credit cards) will take root in economies currently dominated by mobile payments. However, it is not likely that widely available services, like e-commerce, will proliferate in these mobile-money first markets without the development of more functionality in the mobile money payment infrastructure that allows for increasingly complex transactions.

At the core of these improvements is intermediating trust between a buyer and seller who are unknown to each other. The reason cash is so attractive at the point of sale is because it eliminates the need for any trust between the merchant and the customer. The customer sees what he or she wants and the merchant sees the cash. No trust required. When that transaction takes place over distance where neither the customer nor the product is present in the same location, trust is critical to consummating the transaction. Mobile money providers must start to think more carefully about how to build trust into the payment models so the next phase of digital commerce in emerging economies can start to take root.

Mr Firas,

It seems the mobile money operators are too comfortable and have no real competition and are not incentivized to do anything, leave alone improving trust and everything you wrote. These are all great ideas that could really improve the MM system especially scheduled payments, reversals, and trust. The other thing is it’s very slow and long winded to make mobile payments, take case in point Apple Pay, it’s very fast and easy, just double tap and faceID, done. It would be great if these MM providers can take cues from these systems and work on optimizing the speed of transactions. I’m not going to hold my breath though…

Greetings Mr Firas Ahmad

What is your comments on the government intention to introduce levy on mobile money transaction upon sending and withdrawing money. This is going to increase transactions cost if the operator shift the burden to the users by increasing transaction charges to cover up their margin. In my views this is going to affect the ecommerce which is still in growth stage by making it too costfull as many players are using mobile money platform to transact